Why should I choose AnalystNotes?

AnalystNotes specializes in helping candidates pass. Period.

Basic Question 9 of 11

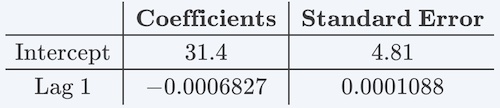

Consider the following output of an AR(1) model.

The mean-reverting level is closest to:

User Contributed Comments 0

You need to log in first to add your comment.

I am happy to say that I passed! Your study notes certainly helped prepare me for what was the most difficult exam I had ever taken.

Andrea Schildbach

Learning Outcome Statements

describe the structure of an autoregressive (AR) model of order p and calculate one- and two-period-ahead forecasts given the estimated coefficients;

explain how autocorrelations of the residuals can be used to test whether the autoregressive model fits the time series;

explain mean reversion and calculate a mean-reverting level;

contrast in-sample and out-of-sample forecasts and compare the forecasting accuracy of different time-series models based on the root mean squared error criterion;

CFA® 2025 Level II Curriculum, Volume 1, Module 5.