Seeing is believing!

Before you order, simply sign up for a free user account and in seconds you'll be experiencing the best in CFA exam preparation.

Basic Question 0 of 10

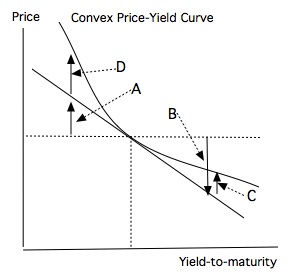

Refer to the following price-yield curve.

The estimated changes due to duration are represented by ______.

User Contributed Comments 2

| User | Comment |

|---|---|

| msusolar | can anybody explain? |

| CFAMay2022 | A&B reps changes in price due to change in YTM/slope of the tangent line (rather than actual changes on curve) |

You have a wonderful website and definitely should take some credit for your members' outstanding grades.

Colin Sampaleanu

Learning Outcome Statements

describe how interest rate swaps are priced, and calculate and interpret their no-arbitrage value;

CFA® 2025 Level II Curriculum, Volume 5, Module 31.